All Categories

Featured

Table of Contents

If these price quotes alter in later years, the company will certainly change the premium as necessary but never ever over the optimum ensured premium specified in the plan. An economatic entire life policy offers a basic quantity of taking part whole life insurance policy with an extra supplementary coverage given with using returns.

Due to the fact that the premiums are paid over a shorter period of time, the costs repayments will be more than under the entire life strategy. Single costs entire life is restricted repayment life where one huge premium settlement is made. The plan is fully compensated and no additional premiums are needed.

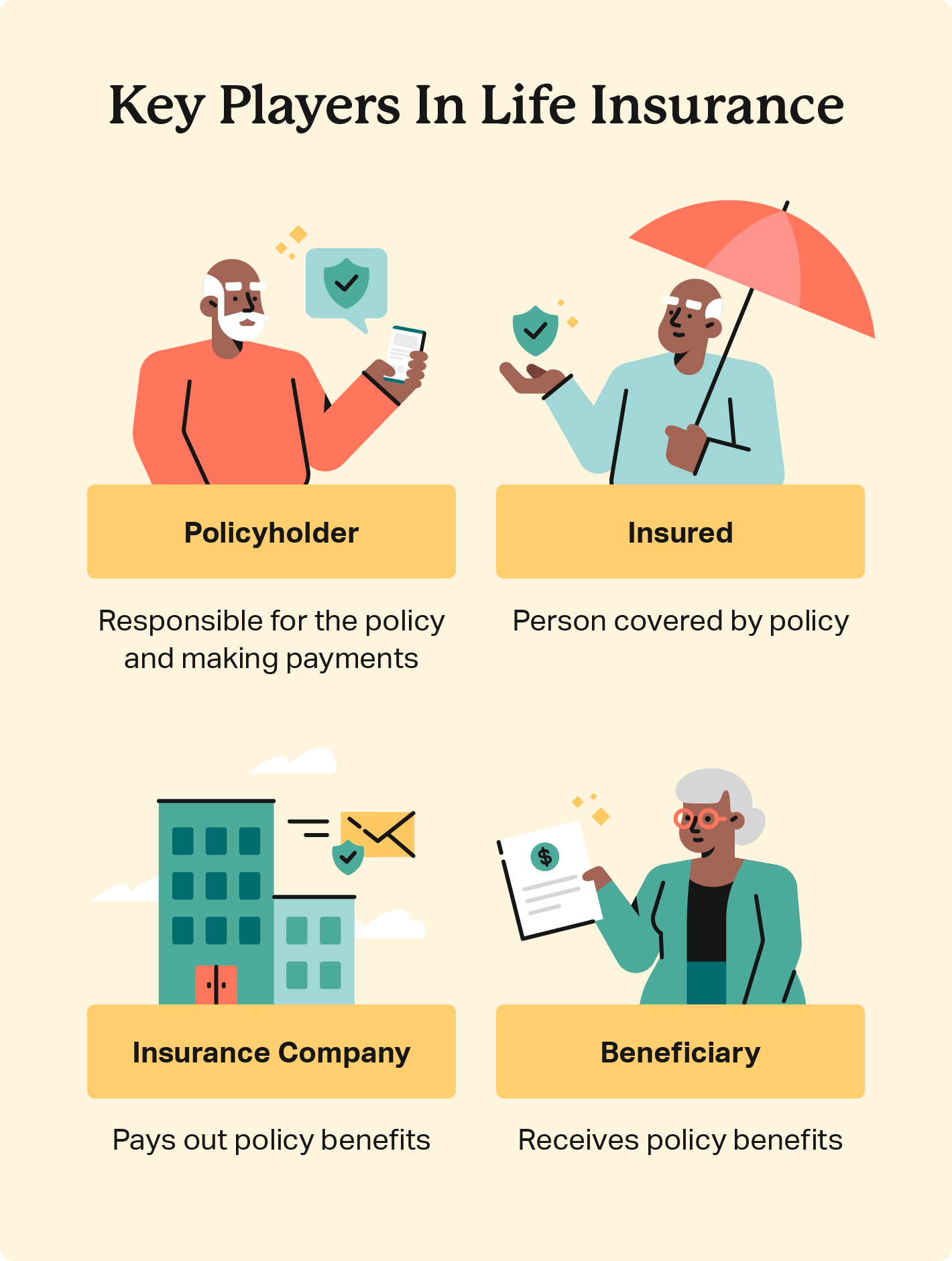

How do I get Policyholders?

Given that a significant settlement is included, it should be considered as an investment-oriented item (Senior protection). Interest in solitary premium life insurance policy is primarily due to the tax-deferred therapy of the accumulation of its money values. Tax obligations will be sustained on the gain, nevertheless, when you surrender the plan. You might borrow on the cash money value of the plan, but remember that you may incur a considerable tax obligation costs when you surrender, even if you have borrowed out all the cash value.

The advantage is that renovations in passion rates will certainly be reflected quicker in passion sensitive insurance than in standard; the drawback, certainly, is that decreases in rate of interest will certainly additionally be felt quicker in passion delicate entire life. There are four basic interest sensitive whole life plans: The global life policy is actually greater than rate of interest delicate as it is made to mirror the insurance provider's present mortality and expenditure as well as passion earnings as opposed to historic rates.

The business credit reports your costs to the cash money value account. Regularly the firm deducts from the cash money worth account its expenses and the cost of insurance protection, usually defined as the mortality reduction charge. The equilibrium of the money worth account collects at the interest credited. The business ensures a minimal rate of interest price and a maximum mortality charge.

How long does Universal Life Insurance coverage last?

Present presumptions are essential to passion delicate products such as Universal Life. Universal life is additionally the most versatile of all the different kinds of policies.

The policy generally provides you an alternative to select one or two kinds of death benefits. Under one choice your beneficiaries received only the face quantity of the plan, under the various other they get both the face quantity and the cash value account - Life insurance plans. If you desire the maximum amount of survivor benefit currently, the 2nd choice must be picked

Who offers flexible Final Expense plans?

It is very important that these presumptions be reasonable since if they are not, you may need to pay even more to maintain the plan from decreasing or expiring. On the various other hand, if your experience is better then the presumptions, than you may be able in the future to avoid a costs, to pay less, or to have actually the plan paid up at an early date.

On the other hand, if you pay more, and your presumptions are practical, it is possible to pay up the plan at a very early day. If you give up an universal life plan you might receive much less than the cash worth account as a result of abandonment costs which can be of 2 kinds.

Death Benefits

A back-end type plan would certainly be better if you plan to maintain protection, and the fee reduces with yearly you proceed the policy. Remember that the rates of interest and expenditure and mortality costs payables at first are not assured for the life of the plan. Although this sort of policy offers you maximum adaptability, you will require to actively handle the plan to maintain adequate funding, especially because the insurance firm can enhance death and expense charges.

You might be asked to make extra costs settlements where insurance coverage might terminate due to the fact that the rate of interest rate went down. The assured price offered for in the policy is much reduced (e.g., 4%).

In either situation you have to get a certification of insurance defining the arrangements of the team plan and any kind of insurance charge. Typically the optimum amount of insurance coverage is $220,000 for a mortgage and $55,000 for all various other debts (Income protection). Credit life insurance policy need not be bought from the company providing the funding

If life insurance policy is needed by a creditor as a condition for making a lending, you might have the ability to assign an existing life insurance plan, if you have one. You may want to purchase team debt life insurance policy in spite of its higher cost since of its comfort and its schedule, generally without in-depth proof of insurability.

What is the process for getting Protection Plans?

However, home collections are not made and costs are mailed by you to the representative or to the business. There are specific aspects that tend to boost the expenses of debit insurance policy even more than routine life insurance policy plans: Particular expenditures are the same no issue what the dimension of the plan, so that smaller sized plans released as debit insurance will have higher costs per $1,000 of insurance coverage than bigger dimension regular insurance coverage.

Because very early gaps are pricey to a company, the expenses need to be passed on to all debit insurance holders. Since debit insurance policy is created to consist of home collections, higher compensations and fees are paid on debit insurance policy than on regular insurance. Oftentimes these greater costs are passed on to the insurance holder.

What does a basic Death Benefits plan include?

Where a company has different costs for debit and routine insurance policy it may be feasible for you to acquire a bigger quantity of regular insurance than debit at no added expense. For that reason, if you are considering debit insurance policy, you must absolutely explore routine life insurance policy as a cost-saving alternative.

This plan is designed for those who can not at first pay for the routine entire life costs yet that want the higher costs protection and feel they will at some point be able to pay the greater costs. The household policy is a combination strategy that provides insurance coverage protection under one contract to all members of your immediate household hubby, other half and kids.

Can I get Riders online?

Joint Life and Survivor Insurance supplies coverage for two or even more persons with the death benefit payable at the death of the last of the insureds. Costs are dramatically lower under joint life and survivor insurance policy than for policies that insure only one individual, given that the chance of having to pay a fatality claim is lower.

Costs are substantially greater than for plans that guarantee a single person, because the likelihood of having to pay a death case is higher. Wealth transfer plans. Endowment insurance coverage attends to the settlement of the face total up to your beneficiary if death occurs within a particular time period such as twenty years, or, if at the end of the certain period you are still alive, for the payment of the face quantity to you

{kind=link}

Latest Posts

Funeral Insurance Definition

Funeral Cost Cover

Universal Life Insurance Quotes Online Instant